Until recently, brands have felt stressed out by the demand to be everywhere. The urgency has felt more like a threat than a strategy for most. It meant one agency for Amazon, another for creative, a broker for retail, a separate team for DTC, and a founder on Sunday night reconciling three P&Ls that told three different stories. Multi-channel was the goal. Chaos was the reality. That era is over.

A new category of commerce partner, the retail operator, has made multi-channel not only feasible but expected. One partner purchases your inventory, becomes the seller of record, and operates every channel with its own capital on the line. The coordination problem disappears, and the excuses disappear with it. If your competitors are already showing up on Amazon, Walmart, TikTok Shop, DTC, and retail shelves with healthy margins, there is no longer a structural reason your brand is not right next to them.

Below, I break down why single-channel strategies stall growth, how the strongest brands build a channel mix where every platform reinforces the next, and why the partner holding your inventory matters more than the partner managing your ads.

Why Single-Channel E-commerce Fails for CPG Brands

Every channel has a ceiling. The brands breaking through right now are the ones building balance rather than picking sides.

DTC-only brands hit a wall the moment customer acquisition costs outpace unit economics. CAC has risen 40% between 2023 and 2026, and DTC repeat purchase rates average just 18.8% across consumables, fashion, and durables. That means most brands are constantly chasing new customers just to stay flat.

Marketplace-only brands watch margins erode as Amazon's effective take rate has climbed from 19% of seller revenue in 2014 to roughly 45% by 2023, between commissions, fulfillment fees, and increasingly mandatory advertising. Retail-only brands bleed cash on trade spend while waiting 90 days to learn whether anything actually moved.

The deeper problem is not the channels themselves. It is how brands organize around them. Most treat each channel as a separate business with its own strategy, its own P&L, and its own messaging. Finance sees one margin story, marketing sees another, and operations sees chaos.

DTC vs. Marketplaces vs. Retail: What Each Channel Actually Does

DTC is your brand lab. Full creative control, first-party data, and complete margin ownership. But DTC growth slowed to 10% in 2024, the lowest in five years. DTC is not a volume play. It is where you learn what resonates.

Marketplaces are where demand converts. Buyers show up with payment saved and purchase intent already formed, which is why significantly higher conversion rates (10 to 18% versus 2.1 to 3.6% for DTC) are standard. Third-party sellers represent 62% of all units sold on Amazon as of Q4 2024. The cost is algorithm dependency, limited customer data, and constant pricing pressure.

Retail is the credibility play. Shelf presence signals legitimacy, and offline sales total 79% of U.S. CPG revenue. But you are giving up 30 to 50% off the top, dealing with long planning cycles, and navigating real supply chain complexity.

The strongest strategies do not treat these channels as competitors. DTC teaches you which messages land. Marketplaces prove which SKUs convert. Retail validates that the brand can move volume at scale. Each one feeds the next.

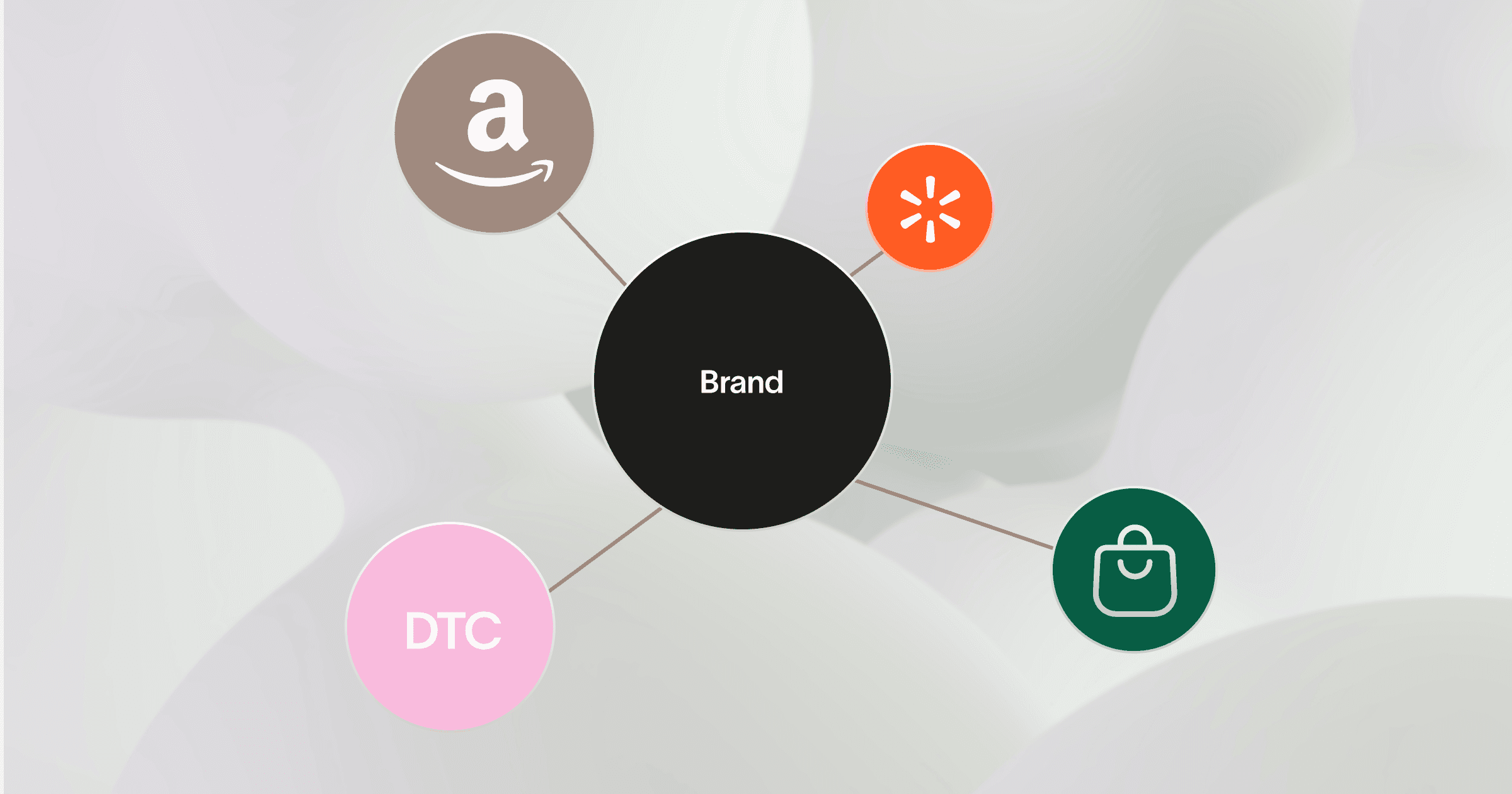

How the Best Brands Build a Channel Mix

IMAGE PLACEHOLDER

How the Best Brands Build a Multi-Channel Strategy

The brands scaling without splintering all share one thing: each channel validates the next. None of them exist in isolation. Here is what that looks like in practice.

From One Channel to Everywhere: Three Paths That Worked

Poppi started DTC to build community, used TikTok virality to prove scalable demand, then moved to Amazon for conversion and retail for mass distribution. Revenue hit $500 million in 2024, and PepsiCo acquired the brand for $1.95 billion in March 2025. The foundation was DTC storytelling that carried through every channel.

Chomps went marketplace-first to own the "healthy protein snack" search on Amazon, then used that conversion data to expand into retail and DTC. By letting Amazon prove demand before scaling outward, Chomps built a channel mix where each platform validated the next. The brand is now the fastest-growing snack in America and on track for $1 billion in sales.

Blueland went DTC-first to educate shoppers on refillable cleaning products. The brand reached profitability by 2023 through DTC alone. By the time they landed in 1,800 Target stores, the brand already had DTC storytelling, Amazon conversion data, and marketplace reviews to de-risk the retail launch entirely.

The pattern is consistent. TikTok drives measurable lifts in Amazon branded search volume, with 22% of sales attributable to TikTok's influence for brands active on both platforms. That cross-channel compounding is exactly what single-channel strategies leave on the table.

Why the Vendor Stack Breaks at Scale

Most brands do not hire one partner to run their entire commerce operation. They hire one agency for Amazon advertising, another for creative, a 3PL for fulfillment, a separate team for DTC, and maybe someone for TikTok Shop. Everyone manages their lane. 98% of sellers multi-channel, and the coordination that requires is something the agency model was never built for.

You have seen it happen. The advertising agency launches a push on a product the 3PL did not know was about to go out of stock. A competitor drops prices, and no one owns the response across pricing, content, and advertising. The DTC email program runs win-back campaigns for customers the Amazon team does not even know exist.

Commerce is an integrated system. Conversion rate affects organic rank. Organic rank affects ad efficiency. Inventory position affects every channel simultaneously. When you manage that through separate vendors, the gaps between them become nobody's job. Your brand absorbs every one of those consequences.

What Is 2P and Why It Matters

What Is 2P and Why It Is the Future of Channel Strategy

So if single-channel stalls growth and the vendor stack breaks at scale, what actually works? The 2P model is a commerce structure where a retail operator purchases your inventory, becomes the seller of record, and runs every channel as its own business with its own capital on the line. It sits between 1P (vendor-controlled) and 3P (brand-controlled) and defines a category of commerce partner that did not exist until recently.

To understand why it matters, you have to understand what it replaces.

Why 1P, 3P, and In-House Models Fall Short

1P (Vendor Central): Amazon buys your inventory and runs your channel on its terms. Pricing, customer relationship, margin: all theirs. Then, in late 2024, Amazon began terminating 1P relationships with thousands of established CPG brands, leaving them responsible for a channel they had never actually operated. 1P was never a strategy. It was a dependency.

3P (Agency): Your brand stays the seller of record. The agency files a ticket. The vendor sends an update. It all lands back on you. Fee-based models, whether retainers, percentage of ad spend, or percentage of revenue, all create the same problem: the agency earns whether your products sell or not. Amazon CPC rose 15.5% in 2025, and the brands absorbing those rising costs are the same ones paying agencies a percentage of the spend driving them up.

In-House: Full control, full visibility, and full cost. Salaries, headcount, and competing for talent that actually knows how to run these channels at scale. Only 11% of CPG companies have achieved significant financial benefits from their digital initiatives. Most teams are stretched thin before they even get to multi-channel.

How 2P Changes the Equation

1P (Vendor Central) | 3P (Agency) | In-House | 2P (Retail Operator) | |

|---|---|---|---|---|

Owns inventory risk | Amazon | Brand | Brand | Operator |

Seller of record | Amazon | Brand | Brand | Operator |

Owns the outcome | Amazon | Escalates to you | Brand (full burden) | Operator (fully) |

Incentive alignment | Amazon's interests | Fee-based (misaligned) | Internal politics | Shared P&L |

Channels managed | Amazon only | Usually Amazon only | Depends on headcount | Amazon, Walmart, TikTok Shop, DTC |

Creative + ops integrated | No | Rarely | Expensive to build | Always |

Brand protection | Amazon's discretion | Billable service | DIY | Core function |

What you pay | Margin to Amazon | Retainer + % ad spend | Salaries + overhead | Purchase orders only |

Neato purchases your inventory at wholesale, becomes the seller of record across every channel, and runs the full commercial system as its own business: pricing, content, advertising, fulfillment, brand protection, and customer experience. You ship product to one destination. One purchase order. One partner. One inventory pool distributed across a national fulfillment network, with 1 to 2 day delivery on every channel.

The distinction that matters most is not operational scope. It is incentive structure. When a retail operator owns inventory, they own the outcome. Revenue comes from selling your products profitably, not from billing hours or marking up ad spend. That alignment changes every decision, across every channel. Brands like Earth Animal, Wiley Wallaby, and Dot's Pretzels have seen triple-digit YoY revenue growth under this model. Not because the tactics changed, but because the incentive structure did.

If your brand is managing a vendor stack that nobody owns end to end, or navigating a Vendor Central transition and need stable operations yesterday, talk to Neato. One PO. One partner. Every channel. Total accountability.

FAQ

What is a multi-channel ecommerce strategy? A: It is an approach where a brand sells through multiple platforms, typically DTC, marketplaces like Amazon, and retail, with unified messaging, pricing, and operations. The goal is not just presence on more channels. It is making sure each channel reinforces the others so growth compounds instead of fragments.

What is the difference between multi-channel and omnichannel? A: Multi-channel means selling on more than one platform. Omnichannel means those platforms are actually integrated, so the customer experience feels seamless no matter where a shopper engages. A true omnichannel strategy syncs inventory, messaging, promotions, and data across every touchpoint.

What is the 2P model on Amazon? A: In 1P (Vendor Central), Amazon buys your inventory and sells it under its own account. In 3P (Seller Central), your brand is the seller of record and manages the channel directly. In 2P, a retail operator purchases your inventory and becomes the seller of record, combining 1P's operational ownership with 3P's channel control and brand visibility. The difference that matters: the operator earns from selling your products profitably, not from billing you.

How is a 2P retail operator different from an Amazon agency? A: An agency manages your account from the outside for a fee. They make recommendations. You make decisions. When something breaks, you own the outcome. A 2P retail operator purchases your inventory, becomes the seller of record, and runs the channel as its own business. The structural difference is skin in the game: a retail operator has its own money at risk. An agency does not.

What are the pros and cons of DTC vs. Amazon vs. retail for CPG brands? A: DTC gives you full creative control, first-party data, and high margins but comes with rising acquisition costs and limited organic reach. Marketplaces provide massive built-in traffic and higher conversion rates but limit customer data ownership. Retail delivers credibility and mass exposure but requires 30 to 50% margin concessions and long planning cycles.

Can a small CPG brand execute a multi-channel strategy? A: Yes, but sequencing matters. Most emerging brands should start with one or two channels, build proof of demand, and expand from there. Trying to be everywhere at once without operational infrastructure leads to channel conflict and margin erosion. A phased approach, often starting with DTC or marketplace, builds the data and systems you need to scale into retail.