Every CPG founder eventually walks into the same debate.

Should we sell to Amazon (1P/2P) and let them resell? Should we sell to consumers ourselves (3P)? Should we run both at once (hybrid)? The conversation almost always gets framed as a financial question. Vendor terms versus seller fees. Net PPM versus contribution margin. MAP enforcement versus pricing flexibility. Spreadsheets get built. Decisions get made on basis points.

I have sat through dozens of these conversations, and I want to make a case that almost nobody makes inside them: this is not primarily a financial decision. The brands that get this wrong don’t lose a few points of margin. They lose strategic control of their largest sales channel — sometimes permanently — without realizing what they traded for what.

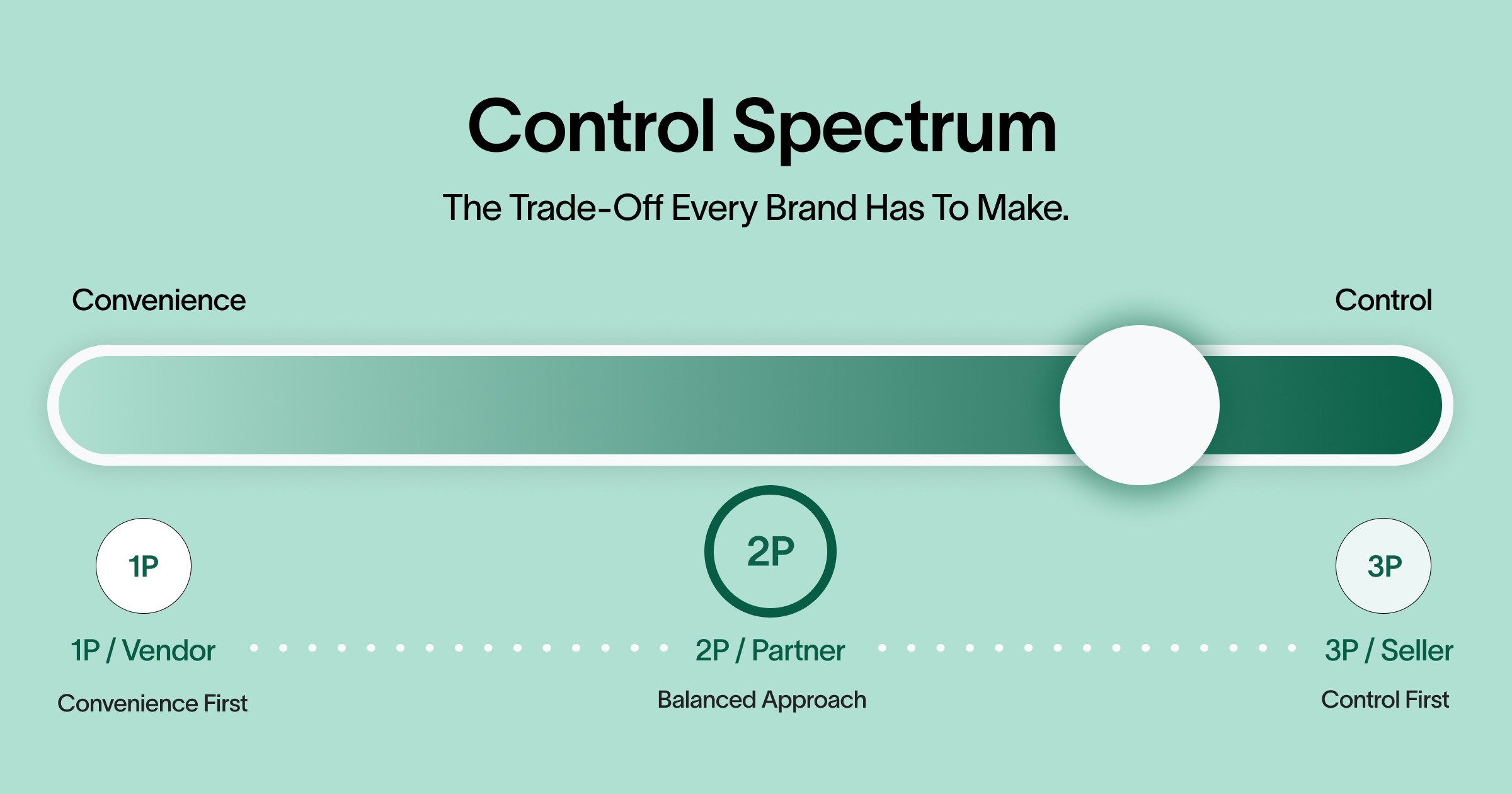

The decision is about control versus convenience. Once you frame it correctly, the right answer for your business gets a lot more obvious.

What you are actually choosing between

Strip away the acronyms. Three operational questions are on the table:

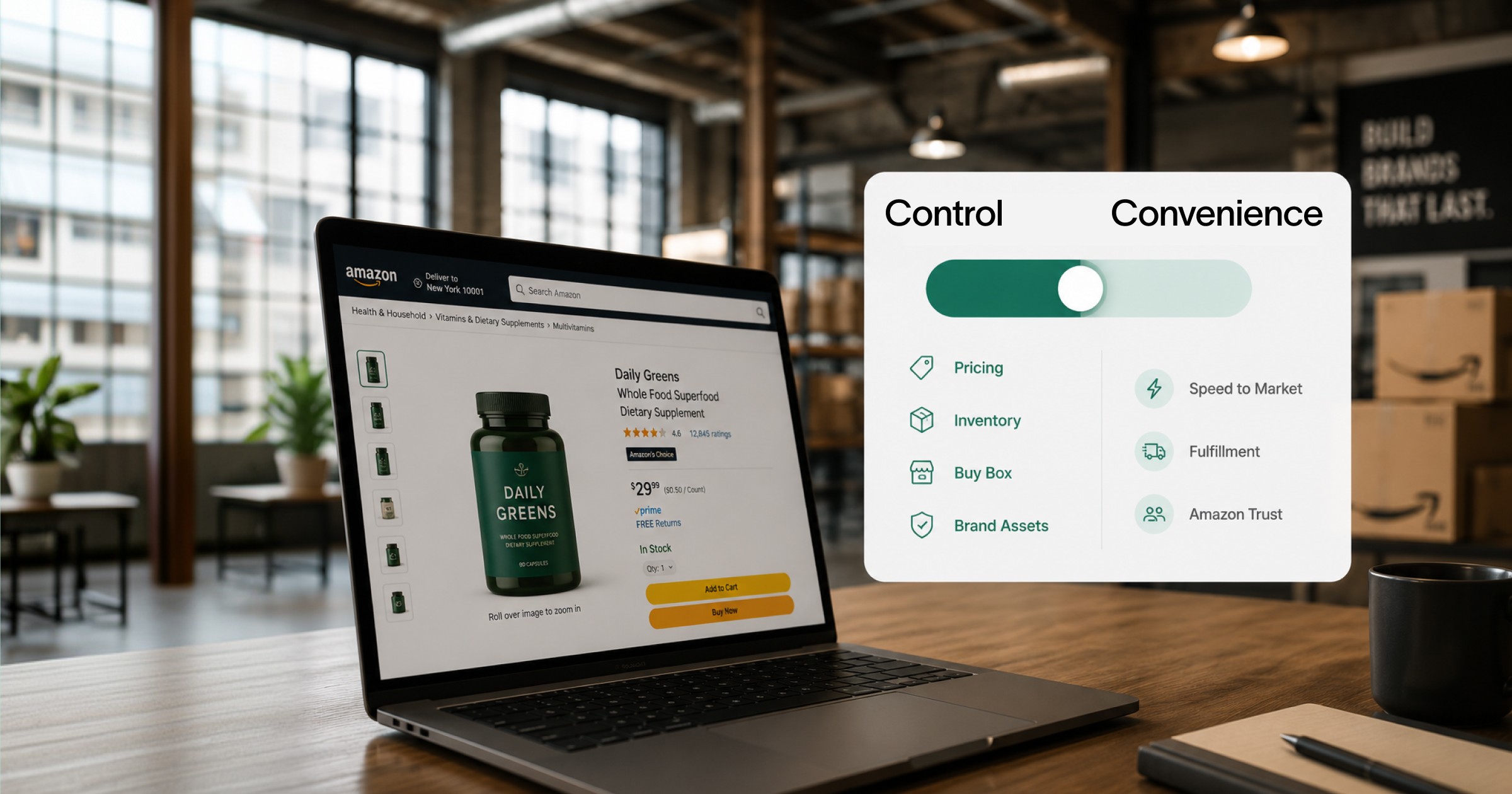

Who controls your price on Amazon — you, or someone else?

Who controls your inventory levels and fill rate — you, or someone else?

Who controls your advertising, your content, and how your brand is presented — you, or someone else?

Every operating model is a different answer to those three questions, packaged with a different bill of operational work and a different risk profile. Most brands optimize the package they receive. The brands that build durable Amazon positions optimize the answers first, then accept whichever package gets them there.

Answers first, package second. That reordering is the entire game.

Pure 1P / Vendor Central: convenience, with a real strategic tax

You sell wholesale to Amazon. They handle pricing, inventory, fulfillment, returns, customer service. You issue POs, fulfill them, collect a check. Operationally, this is the lightest model in retail. Strategically, it is the heaviest tax in the marketplace.

Amazon owns your retail price. Amazon owns your in-stock decisions. Amazon decides whether to promote you, discount you, or quietly stop reordering. You can ask. They can decline. The negotiation leverage is asymmetric, and the asymmetry isn’t in your favor.

Brands go pure 1P for the simplicity. Eighteen months in, many discover the simplicity has cost them the ability to run their own brand strategy on their largest channel. The check still clears. The control is gone. By the time the leadership team realizes this, switching costs are real and the runway to rebuild is shorter than they thought.

There are brands for which 1P is the right answer. They tend to be ones with bigger strategic priorities elsewhere who genuinely cannot afford the operational depth of running marketplace themselves. The decision becomes wrong the moment the brand starts treating the convenience as free.

Pure 3P / Seller Central: control, with the full operating bill attached

You sell directly to the customer through Amazon’s marketplace. You own pricing. You own inventory. You own ads. You own content. You also own the entire operational stack: forecasting, FBA shipments, customer service, returns reconciliation, account health, IP enforcement, listing hijackers, and the suspension that lands at 11 p.m. on a Friday.

3P done well is the highest-leverage model in modern consumer goods. 3P done poorly is a brand quietly hemorrhaging margin while leadership pretends the Amazon team has it under control.

The misread that makes 3P fail is treating “we have a Seller Central account” as the same thing as “we are running a 3P strategy.” It isn’t. It is the start of an operational liability that does not pay off until you build the depth to match the model. Half-built 3P operations destroy more brand value than 1P does.

Hybrid: usually the worst of both, occasionally the best of both

Hybrid is supposed to combine the strengths — sell some SKUs 1P for stability, run others 3P for control. In practice, most hybrid setups inherit the weaknesses of both models without compounding the strengths of either.

The classic failure pattern: brand sells the same SKU 1P and 3P at once. The 1P listing wins the buy box at a price that breaks the 3P unit economics. The 3P version gets suppressed. The brand is now paying for advertising that drives traffic to a listing it doesn’t really own. Margin evaporates. Nobody understands why.

Hybrid can work. It works when the brand has clear, defensible logic for which SKUs live in which model and the operational discipline to enforce that logic at the buy box level. It rarely works by default.

The right frame: control vs. convenience

For every SKU, every category, every brand, the real question is the trade-off:

How much operational complexity are we willing to absorb in exchange for strategic control?

How much strategic control are we willing to surrender in exchange for operational simplicity?

Both ends of the spectrum are legitimate. A capacity-constrained brand with bigger fish to fry can rationally choose convenience and accept the cost. A brand whose Amazon presence is a meaningful share of total revenue cannot rationally hand strategic control to a partner whose interests are not aligned.

The mistake isn't picking one model over another. The mistake is making the call on the wrong axis. Choosing 2P "because the math looked better in the spreadsheet" is exactly how brands wake up two years later wondering why their largest revenue source is being run by someone who has never met them.

What "2P done right" actually looks like

Most 2P relationships are structured as a glorified Vendor Central — a partner buys inventory and decides almost everything else. That model has all of 1P's strategic problems with one less middleman.

The 2P that actually wins is structurally different. The brand keeps the strategic decisions: pricing posture, channel mix, advertising philosophy, NPD priorities. The partner takes on the operational stack — and is structurally aligned around the brand's success on Amazon, not around extracting margin from the brand. Different incentives produce different decisions. Different decisions produce different outcomes.

The acid test for any 2P arrangement is one question: who decides what happens when a competitor undercuts our price by 12%? If the answer isn't "the brand and the partner together, in a conversation that takes hours and not weeks," you don't have a control structure. You have a vendor with a different invoice line.

The takeaway

2P, 3P, and hybrid are operating models. They are not strategies. The strategy is how much control you intend to keep over the largest channel in your business — and how much operational weight you are willing to carry to keep it.

Pick the trade-off that matches the business you're trying to build. Then pick the model that delivers the trade-off. Doing it in the other order is how brands lose Amazon without ever realizing they handed it away.